How Morgan Stanley, UBS, Wells Fargo, etc. take advantage of average everyday clients and employees to feed the bottom line…

Retail investment managers manage investments for everyone from the blue-collar worker making $50k/year to the big wig CEOs pulling millions. The retail investment managers we speak of are the bulge bracket banks, or the “wirehouses” – e.g. Merrill Lynch, Wells Fargo, Morgan Stanley, Citigroup, UBS, etc.. They all have have retail divisions of Private Wealth Management which employ Financial Advisors. FA’s are mainly employed in retail branches around the country, not at the bank’s headquarters.

The big banks, Financial Advisors they employ, and their clients are the players in the numbers game we’re about to describe. We’ll use the fictitious Fargo Stanley as a proxy for a typical bank’s retail investment management division. Fargo Stanley (FS) starts the game by hiring young or first-time finance professionals with little to no financial experience. Hiring younger Financial Advisors for FS is similar to buying lottery tickets. The requirements are a college degree, proving you can have a conversation in the interview, and lastly mentioning something about having rich friends or family members so the interviewer believes that your network includes $$$$$$. How about one’s ability to manage investments or knowledge of financial markets? Doesn’t matter. In fact, the interviewer lets the candidate know that 95% of this role is sales, not investment management. Instead of investment management, from the moment a Financial Advisor is interviewed, asset acquisition is the focus.

Since FA’s are selling investments, they are required to obtain a Series 7 license. The curriculum goes over textbook investment management basics, nothing more, nothing less. Fargo Stanley’s approach to passing the Series 7 exam further shows how banks hires salespeople instead of those with investment management potential. Each new hire must pass the Series 7 within 3 months of being hired (immediately fired if you fail). The same bulge bracket banks – which house investment banks – hire college grads from more prestigious backgrounds for their investment banking or Sales and Trading analyst programs. These new hires also must pass the Series 7…within 1 week! If the relatively easier interview doesn’t show it, this should exhibit the lower standards banks hold for FA’s. And the reason for this is that banks churn through FA’s, while analysts are hired to be long-time employees.

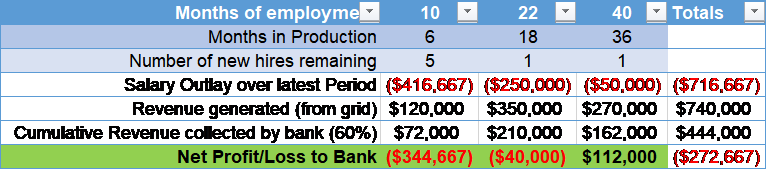

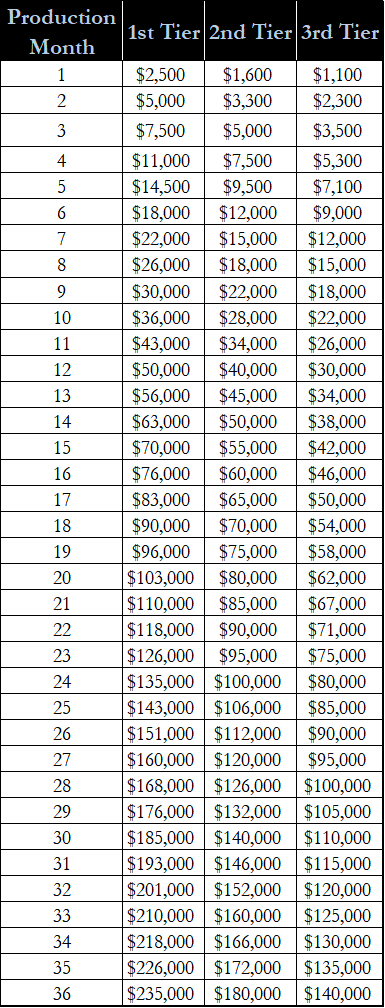

Those FA’s that pass the Series 7 are “revenue producing” junior FA’s within 4 months. The main difference between junior and regular FA’s is that junior FA’s have monthly revenue goals (see an actual grid from an unnamed bank in Figure 1 at the end of this article). Another difference is that junior FA’s are given a salary which is gradually decreased to minimum wage if they make it to the end of the 3-year program. These numbers (from 2017) are similar across the country and across each bank. (FYI, I can stand by these numbers because I used to work for one of these big-name brokerage shops and compared with peers across almost every bank.) Junior hires rarely make more than $60k/year, and most are around $50k. We’ll see why it doesn’t matter if Fargo Stanley’s hiring class size is 1 or 100 over time. Half of new hires are cut within the first 6 months, and the rest are gone by the 2nd year of production. Given those facts, on average for every ten people hired, Fargo Stanley pays a NET total around $220k (after subtracting the average revenue produced by the average junior FA). Computation is in Figure 2 below. That populates to $270k for 10 lottery tickets, and we’ll see how a 10% success rate translates to a huge payoff for Fargo Stanley.

Figure 2: 10 new hires = $270k (winning) lottery ticket

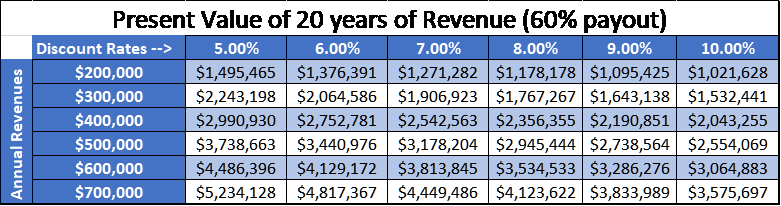

Anyone who makes it through the 3rd year of Fargo Stanley’s training program must generate $150k in annual revenue. Additionally, since this is more than the declining salary, FS is not responsible for salary going forward (because they pay you from your own revenue after the first 3 years). The Financial Advisor is entitled to 40% of the total revenue collected from clients, while FS takes the rest. Figure 3 shows a sensitivity analysis of a range of annual revenue streams using different discount rates over a 20-year span. For those unfamiliar with discounting cash flows, we are computing the “present value,” of 20 years of revenues. Normally FA’s strive to grow revenue and reach $1mm in gross annual revenue. So, $400k average revenue for this golden goose over a 20 year span would err on the side of extreme caution and conservativism. It’s clear to see the value in the $270k of lottery tickets.

FIGURE 3 – What 20 years of annual revenue is worth in today’s dollars

Churning through underqualified employees as a lottery ticket is just the start of the industry’s problem with retail investment managers. As mentioned, a new hire’s requirements to avoid getting laid off are so tough that 90% fail. New hires need to bring in money and revenue so quickly that raising assets is not just the #1 concern over the first few years, it is the only concern. Junior FA’s are so concerned with revenue – increasing the number of clients – that they have no time to manage investments and are forced to put their clients in a pre-determined “non-discretionary” platform where Fargo Stanley chooses all of the investments. In every office-wide meeting I sat through as a Financial Advisor, management’s only objective was to convince Advisors how to meet potential clients and get their money into Fargo Stanley. When junior FA’s voiced concerns over actual investing, the managers in charge of the meeting would encourage them to allocate client portfolios to Fargo Stanley’s “non-discretionary” platform while charging the highest annual fee possible. Fargo Stanley has intelligent people deciding how the non-discretionary platform is allocated, so this doesn’t seem like it’s that bad at first glance. Except once you find out that FS is in bed with the asset managers whose funds on this platform. There is a flow of money between FS and asset managers as both entities are benefitting from the relationship; this is called “revenue sharing.” Fargo Stanley gets kickbacks as they allocate more funds to managers in revenue sharing agreements. Of course, the client is paying these fees as part of a funds “expense ratio,” in addition to the management fees or commissions going to FS. After the layers of fees, subpar performance is almost guaranteed in these non-discretionary investing platforms. I have not seen a single one which has not trailed its benchmark. For more on revenue sharing, here is an excerpt taken from Morgan Stanley’s disclosure document:

Morgan Stanley charges each fund family we offer a mutual fund support fee, also called revenue sharing, up to a maximum per fund family of 0.16% per year ($16 per $10,000 of assets) on the mutual fund holdings of our brokerage account clients. The minimum annual fee is $250,000 per fund family but may be reduced in certain circumstances. Revenue sharing payments are in addition to the sales charges, annual distribution and service fees (referred to as “12b-1 fees”), applicable redemption fees and deferred sales charges, and other fees and expenses disclosed in the fund’s prospectus fee table.

In addition, Fargo Stanley (back to the hypothetical bulge bracket bank) has other departments – Investment Banking, Research – which have relationships with hundreds of publicly traded companies. As you guessed, FS’s research on these companies has a huge positive bias. The “information” which your FA uses to make “informed” investment decisions is just as biased as the “non-discretionary” platform’s investment recommendations. (Quick tangent coming up…) To avoid this obvious conflict of interest, you could find a Registered Investment Advisor which is categorized as a “Fiduciary.” These businesses are less likely to have such obvious conflicts of interest. My personal belief is that more money will flow into RIA’s as people are becoming weary of incessant fees and subpar performance from large firms.

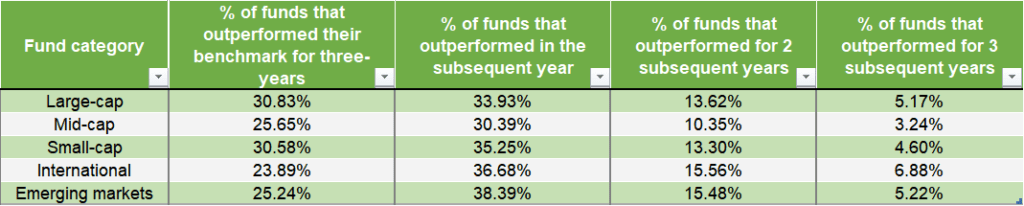

Avoiding a complete tangent, let’s go back to Fargo Stanley’s non-discretionary platform. FS’s Financial Advisor is going to speak highly of their non-discretionary platform because this is how they have been trained. Instead of teaching its Financial Advisors how to invest on their own, FS only trains employees how to convince clients that fees and underperforming investments are not reasons to take your money elsewhere. In other words, training concentrates on attracting clients to below average portfolio returns, and keeping clients there if they ever discover the truth. Every retail investment shop convinces its employees that their investing platform is the best, when in fact they are all equally mediocre. See Figure 4 below for evidence of how selecting winning funds is a waste of time. Out of all the actively managed funds, only about 25-30% will outperform their benchmark over 3 years. After that it gets really ugly– one fifth of the remaining – only 5-6% will outperform their benchmark over the subsequent 3 years! This tells you one thing, if the benchmark wins 95% of the time, then you should just invest in the benchmark. More on this when we cover why passive investing is better than active investing for retail clients.

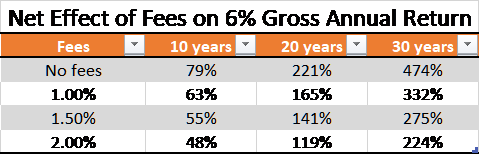

For those of you who believe your Financial Advisor provides a great service even though his/her company is evil, we have to burst your bubble. We already discussed the fact that retail investment managers knowingly hire people who have no little to no relevant investing background. Then we highlighted how their training has nothing to do with investing, instead it concentrates on sales skills that you would find in a used car lot. The best FA’s have trained you to ignore investment performance and your 1-2% management fee. They send you fancy birthday cards, Christmas cards, and butter you up so you feel bad about leaving them. In fact, if you get cards and gifts in the mail, I guarantee your Financial Advisor is overpaid. You probably have below average returns which have been covered in salesmanship. Unfortunately, for most of you in this case, you will probably not leave your FA because you want to avoid the difficult conversation. In case numbers talk, see Figure 5 below. Here you can see the effect of your FA’s annual fees on your long-term returns. The table directly below shows how 2% in management fees can cut 30 year returns in half! Further below, we’ve included a calculator where you can see the effects for yourself.

FIGURE 5 – The compounding effect of fees is where banks get rich while clients get the shaft

We do realize that many people need a Financial Advisor for their own specific reasons; and in that case FA’s obviously need to be paid and the same applies for the companies that employ them. That being said, in the near future we’ll write more on who can best manage your money if you do need a Financial Advisor (quick and dirty answer – RIA’s), and who to go with if you don’t need a Financial Advisor.

Takeaway: Retail investment management shops, active investing, and birthday cards from Financial Advisors are sucking the profits out of your investments. The industry is designed to capitalize from deterioration of clients’ investment returns.

FIGURE 1 – Junior Financial Advisor Revenue Grid – 3rd Tier required to stay in program (under 3rd Tier = Do Not Meet. Greater than 3 consecutive DNM’s –> you’re fired)

Since active management saw 25% decline in AUM in 2016, is there a possibility that jobs like Financial Advisors under Retail investment/private wealth management may not exist in future as more people would diverge in passive/ETFs?