HEADLINE: “US BANKS LAY OFF 80% OF SALES & TRADING STAFF”

That’s something we won’t hear anytime soon. As unlikely as the headline seems, history has already proved it true.

It’s no secret that the S&T industry has been on a decline. “Since the financial crisis” is usually what you hear at the end of that phrase…that’s just some bullshit reasoning, political spin, call it whatever you want. Let’s look at the facts – trading floors such as the CME, CBOT, NYMEX, and even NYSE are not relevant (at best). Most don’t even exist anymore. This is for the same reason that S&T is going to the graveyard. Investors and money managers only needed a middle man (sales trader) to access product. So when securities were only traded on an exchange floor, you had to go through brokers/floor brokers (equivalent of S&T salespeople).

NY Stock Exchange then

Marijuana smokers need a middle man or drug dealer to access weed, until the markets allowed them to access it directly. Ignore the legalizing of marijuana here, for the same reason I’m asking you to ignore the 08/09 Financial Crisis or Dodd Frank’s effects on S&T. Floor traders were essentially no different from sales traders sitting at a bank in front of a Bloomberg terminal. Floor traders were the end drug dealer while the guy you called at the bank was your buddy who knew the dealer. Once sales traders at a bank could access markets on their computer screens, they didn’t need to go to the trading floor to buy/sell securities. This should start sounding familiar for all the longtime weed enthusiasts – once you got the dealer’s # you didn’t bug your friend for a connect. Continuing that movement towards efficiency and elimination of bottle necks – money managers and investors are increasingly accessing those markets through their own computer screens. It’s like going to MedMen to pick up your chronic fix. That being said about weed, let’s go over some other specifics as far as products go.

NY Stock Exchange now

EQUITIES – I worked on the Equity Sales Trading desk at Goldman Sachs, just as the Financial Crisis started to rear its head in 2007. A couple years later in MBA school, I had to network my ass off to get an internship and then a job. So, I reconnected with some former coworkers at GS….or better yet, I tried to reconnect. One of the only people still working there was an MD, and he told me that GS combined the domestic and international trading desks. Goldman laid off half of its sales force and everyone remaining doubled their workload. Double the workload did not come with double the compensation though. The banks are trying to save money, aka make more money. So, what they do is fire the most highly compensated employees and keep the cheaper/younger workers. Essentially, this has become the cycle in all of the banks. You start there as an undergraduate, work for 5 years and your salary does not reflect your workload. So, you leave the bank and pursue trading somewhere else (the buy-side if you’re really good), go to grad school, or venture into other industries. Meanwhile the bank just replaces you with some kid at half the price, and so on.

Let’s take a step back, while we stick to the equity theme. We just mentioned one of the many ways that the Financial Crisis impacted S&T, but recall that we need to ignore The Crisis to get to the bottom of the dying industry. My point is that these layoffs were going to take place anyway. You can trade almost any stock in the US from your computer or even cellphone. It was the advent of over-the-counter trading and technology which made it possible for money managers to ditch their sales traders. The continuation of this trend has practically led to the disappearance of Domestic Equity Sales desks in America. You still need salespeople for stocks you can’t access though, and therefore international equity sales is barely alive….but this is headed in the same direction. Stocks are like commodities, in that MSFT is MSFT and the security is standardized with no confusion. That makes it easier to trade from a computer and without a salesperson. Take bonds though, and these are not as clean cut.

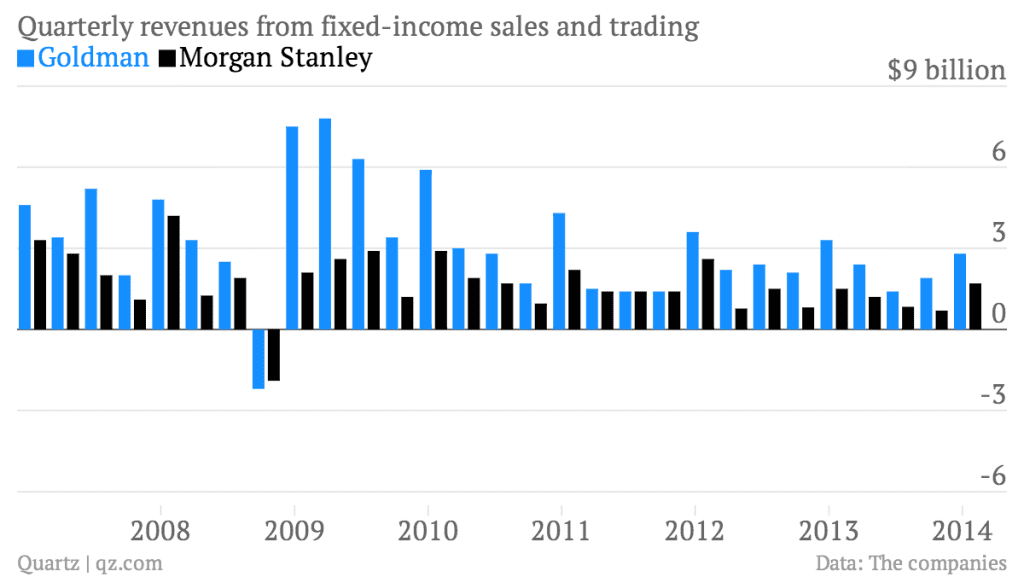

FIXED INCOME – Bonds aren’t as plain vanilla as common stocks. They have different maturity dates, coupons, and capital structures which make them look more like “MSFT 4.2% 2019”, instead of MSFT. Still, this bond is a popular issue and can easily be traded from computer screens. When I worked in Fixed Income Sales at Morgan Stanley, our clients would trade millions in go-go bonds (commonly traded liquid issues) for companies such as Exxon Mobil, GE, or Intel, etc. There was no interaction with the client for these trades. Clients had access to Morgan Stanley’s platform on their computers and could trade on their own. This would amount to commissions as paltry as $10 for a $10mm trade. We would only be able to charge a mark-up, or generate up to 2-3% commissions, if the client wanted to trade a bond which was not accessible on their platform. This was only the case with certain corporate bonds which were illiquid or esoteric, or an entirely separate asset class – structured products.

Asset-backed securities, mortgage-backed securities, collateralized mortgage obligations….and so on with abbreviations such as ABS, MBS, CMO, CMBS, RMBS, CLO….these are the more complex investment vehicles created to securitize debt, They facilitate even more borrowing and lending in the financial markets. From a Sales and Trading aspect, we don’t need to delve into the complexities of these instruments or differentiate between them. These fixed income animals look like SDART 2014-3 B or FN AM9253, and they are also moving towards standardization through OTC trading on computer platforms. A lot of agency MBS or CMO’s can be traded through computer trading platforms though, and this trend will continue. Of course, anomalies in the market will always be present so a human sales trader will be necessary. But, literally one human might be necessary. These sales traders are starting to become and will inevitably be anomalies themselves. Entire desks of traders have been and will continue to be replaced by technology.

Interest rate products such as fixed vs floating swaps, indexed swaps, and derivatives such as swaptions and interest options are another animal of the very broad Fixed Income market. There are more common or more vanilla instruments which are liquid and traded on screens just like those mentioned above. And there are more specialized interest rate products which require human interaction. For example, I had a client who wanted a swap in which one side would reflect a consumer credit default index (http://us.spindices.com/indices/specialty/sp-experian-consumer-credit-default-composite-index). Every swap has a price, for the right quantity, and my coworkers at Morgan Stanley were able to originate this swap as long as it was for a minimum of $2mm. These types of situations are common enough that the anomalies of S&T desks will always be around. Just not very large desks, and the duties of these individuals will be much broader than those of today’s sales traders.

EVERYTHING ELSE – Currency, commodities, options, futures, and derivatives of all types. Commodities by definition are standardized, and that’s why the Intercontinental Exchange (ICE) and Chicago Mercantile Exchange (CME) have killed off the remnants of exchange trading floors. Check out this comic strip for a good visual. It’s all about making money and they are making a ton of it. Now that they don’t need humans making markets and facilitating trading, volumes go through the roof and overhead plummets. The story for “everything else” is much of the same as we mentioned for stocks and bonds. Whatever is simple and plain vanilla is already traded on computer screens with no need for human sales traders. Currencies, commodities and their options firmly fall under this umbrella. Derivatives and more specialized products created for specific client needs would require human interactions.

Specialized products might be the only reason sales traders could exist well into the future; though they will more than likely be responsible for more than just S&T. One more note on “everything else.” S&T for algorithmic trading is quite different from our discussion of products so far. This is based on computer programs developed for high frequency trading (HFT) or some market making programs or…who knows what. I’m not familiar enough with algo trading to describe it better than that, but all you need to know is that it’s based on computer trading. This might be the only area of S&T which grows – both in revenue and headcount. Algo sales trading desks provide the infrastructure, programs, and means for asset managers to access exchanges and even develop their own programs. Of course, there could come a day where asset managers go directly to the exchange and avoid the S&T middle man, as with every other product we’ve discussed. In my opinion this is unlikely because the overhead or infrastructure will probably remain a barrier for money managers. Programmers, or computer science majors, could be highly coveted for these roles in the future. As with anything in modern Finance though, I would recommend pursuing some level of competency in computer programming because that is where the entire industry is going.

Now that you’ve forgotten about the Financial Crisis, Dodd-Frank, and their effects on S&T….do you see why it doesn’t matter? Sales traders are part of the inefficiencies and bottle necks in trading. Banks want to make as much money as possible, so they will adapt to markets by going to the cheapest revenue generators around. I spent little time on political/legal impacts so far because the nature of the business is what drives free markets. Trading is all about efficiencies, free markets…Smith’s Invisible Hand.

It’s true that Trump’s deregulation of banks and scaling back of Dodd-Frank, or lower capital requirements will open up revenue opportunities within Sales & Trading, but this will be temporary. The move towards computer screens and removal of middle men is in the banks’ own interest. Clients will flock to more efficient means of trading. It’s worth noting that there should be a bump in trading revenue across banks, in addition to a bump in hiring as banks are allowed to carry more inventory to meet client demand. This will be temporary as the boost in hiring and revenue will be greeted by even more of a need to reduce expenses within banks. The death of Sales & Trading might be an exaggeration, but S&T will be an anomaly of banks’ revenue generating departments soon enough.

I just started on Goldman Sachs S&T this summer and the MD that hired me “resigned” along with 3 other high level resignations. I don’t want to mention which desk, but I think it seems like this article is spot on.

Jonny, this call of “death” is a bit overplayed. But big earners are going to get cut so don’t look forward to 7 figure paydays while you’re there.

You guys are all f’ed, trading is dead.

A couple months back I attended an event where the speaker mentioned how everyone wants to get into S&T these days. If that speaker (JP Morgan’s recruiter btw) is to be believed then why do people even want to get into S&T when there’s 90% chance that they’ll be fired in a year or two? Shouldn’t they instead start their career from a relatively less known investment firm and work their way up?

Yes and no – starting in a bulge bracket trading shop is a great stepping stone. It can lead to buyside positions, research, or other positions within a bank. If one thinks they want to be a sales trader for their life – then they should do some reflecting because this is not a good long-term career choice. BUT, it is a great way to learn the markets and witness buyside activity from the opposite side.